|

The Commission considered an application by Sheraton Textiles Holdings (Pty) Ltd (“Sheraton” or “the Applicant”), for the amendment of certain existing rebate items under rebate item 311.42 as well as the creation of rebate provisions on woven fabrics and other fabrics classifiable under tariff subheadings 55.13, 55.14, 5903.20, 5212.1, 5212.2, 53.09, 5512.1, 55.16, 5903.10.90 and 5903.90.90 used in the manufacture of goods classifiable under tariff headings 63.02, 63.03, 63.04 and 94.04. During its deliberations and in arriving at its recommendation, the Commission considered the information at its disposal, including comments received during the investigation period. The Commission found that: a) There may exist local manufacturers of the subject fabrics, namely: Svenmill, Mungo and Finlam Textiles. It should be noted that the subject fabrics have never been utilised by the Applicant or industry players within the home textile sector as the current level of duty makes it unviable to compete with finished imported goods.

c) Comments received from industry and labour, suggest diverse views. On the one hand, Texfed, which represents the textile mills, supports the change in scope and description of existing tariff headings under rebate item 311.42, on the other hand it opposes the inclusion of additional fabric tariff headings. d) Svenmill submitted that it manufactures the subject fabrics except for fabrics classifiable under tariff heading 59.03, but failed to provide information pertaining to its production capacity and volume of the said fabrics. e) SACTWU argues that fabrics classifiable under tariff heading 59.03 are manufactured locally by two firms, namely: Mungo and Finlam Textiles. It should be noted that Finlam Textiles make use of rebate item 311.41 to import yarn for the manufacture of fabric classifiable under tariff subheading 5903.90.50 for the automotive industry. f) Mungo submitted that it weaves 100% linen fabric under tariff heading 53.09, which it uses to manufacture a bedding product range, which is a premium product range manufactured to the highest standards, but failed to provide information pertaining to its production capacity and volume of the said fabrics.

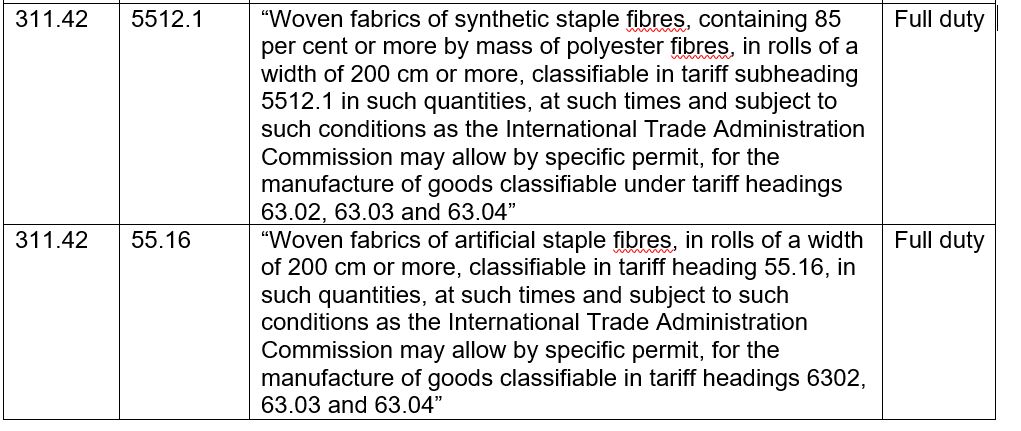

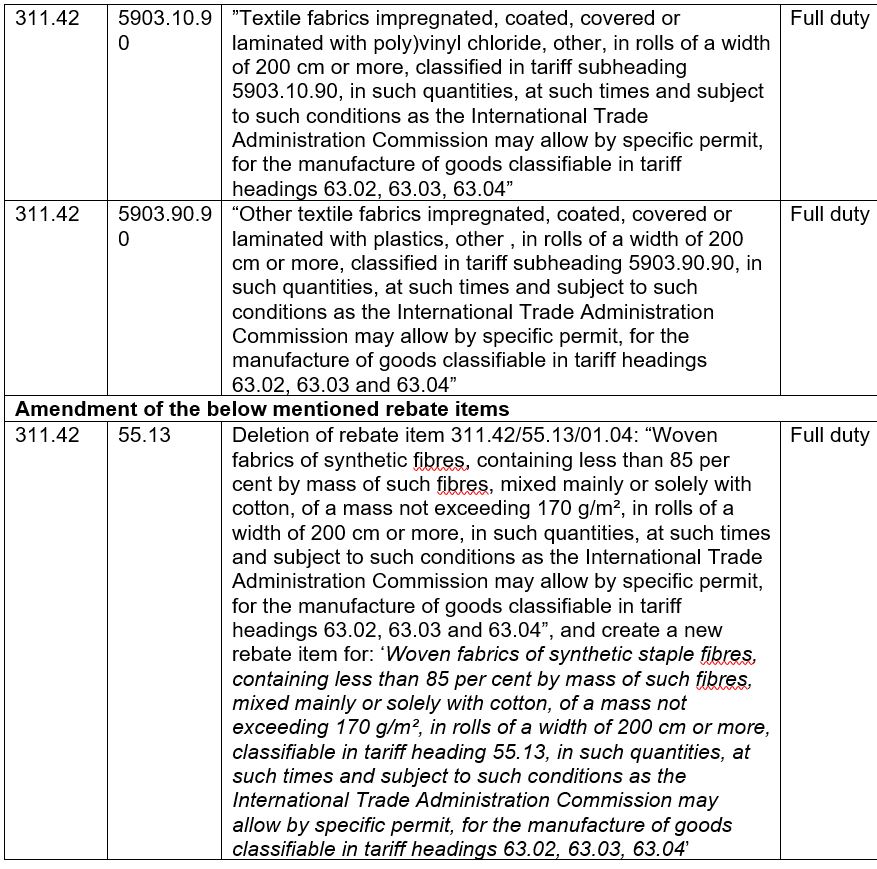

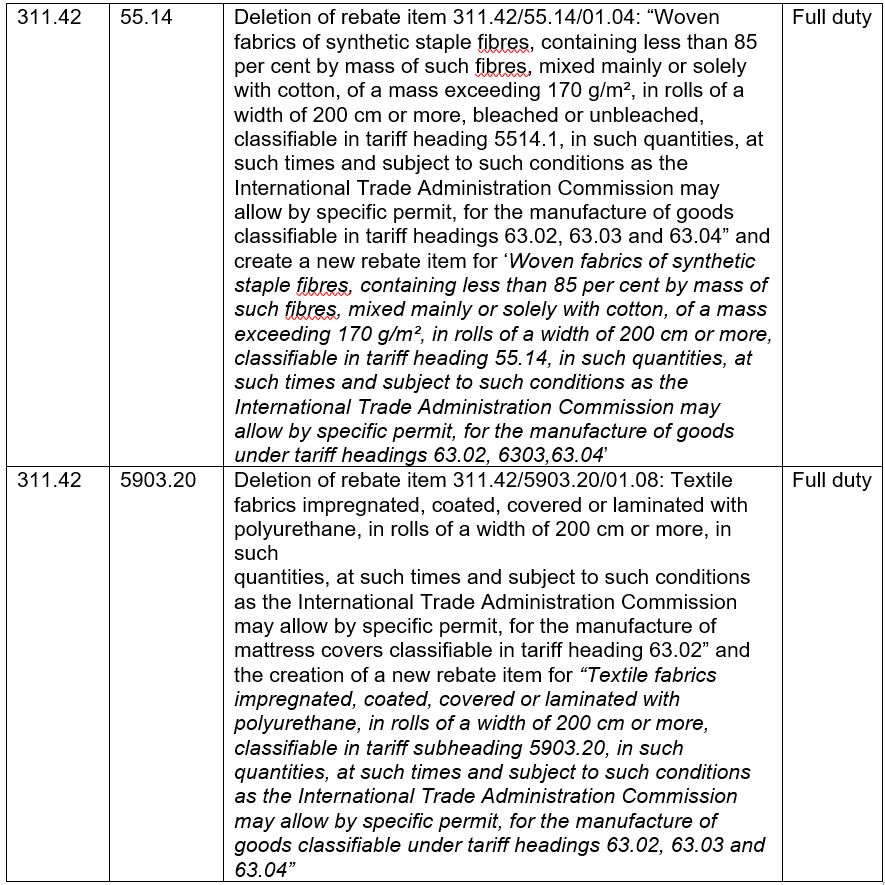

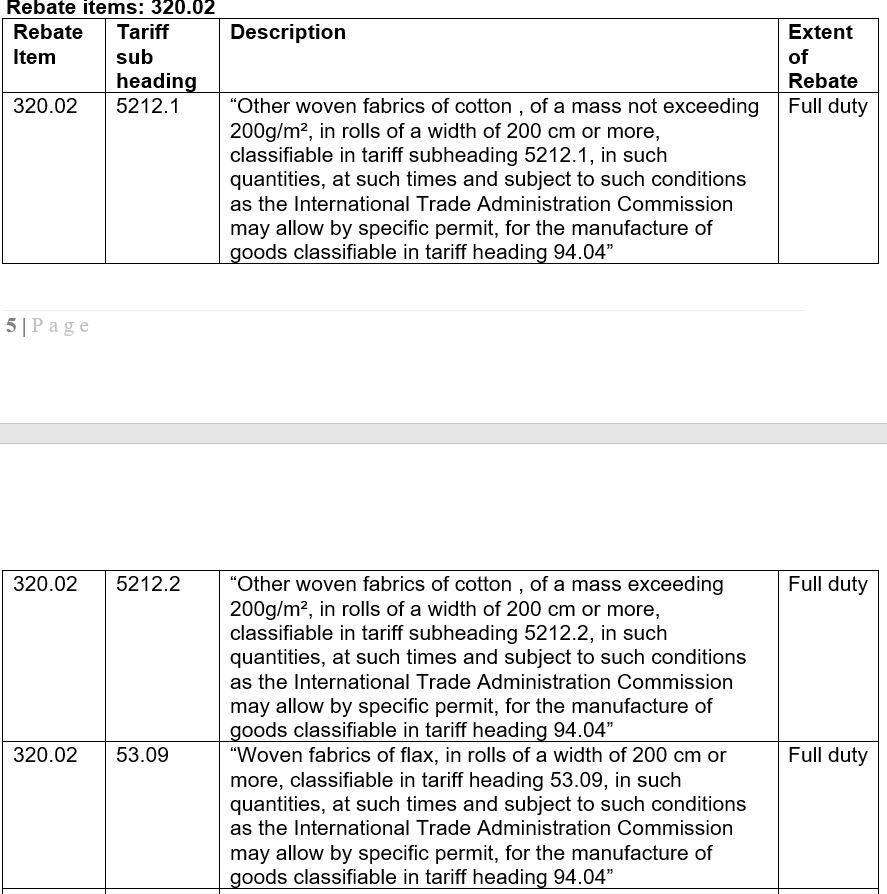

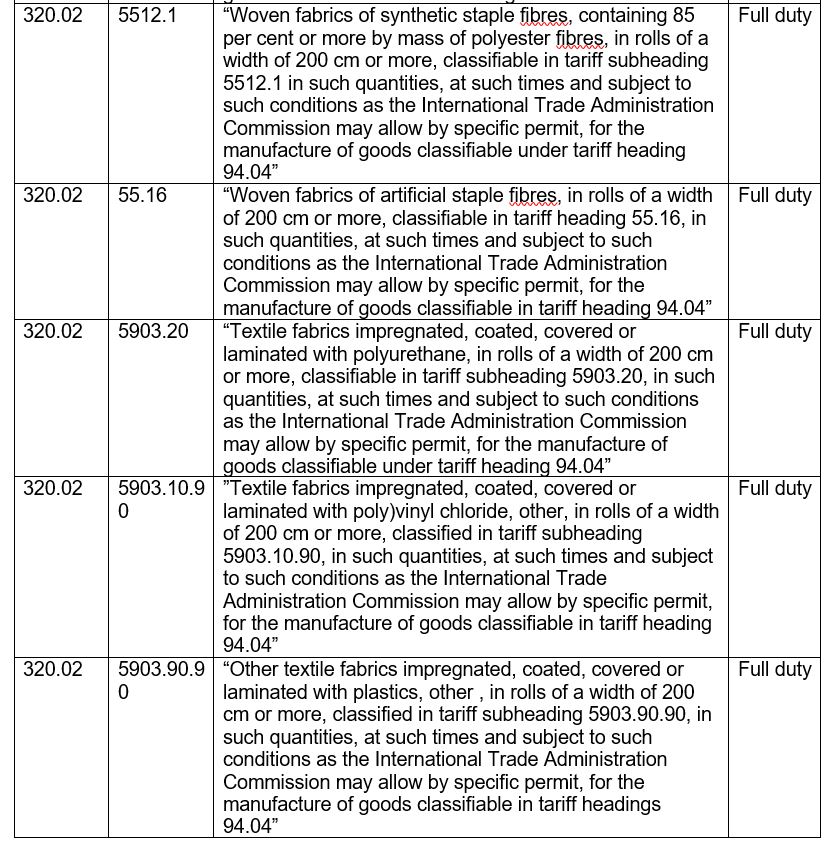

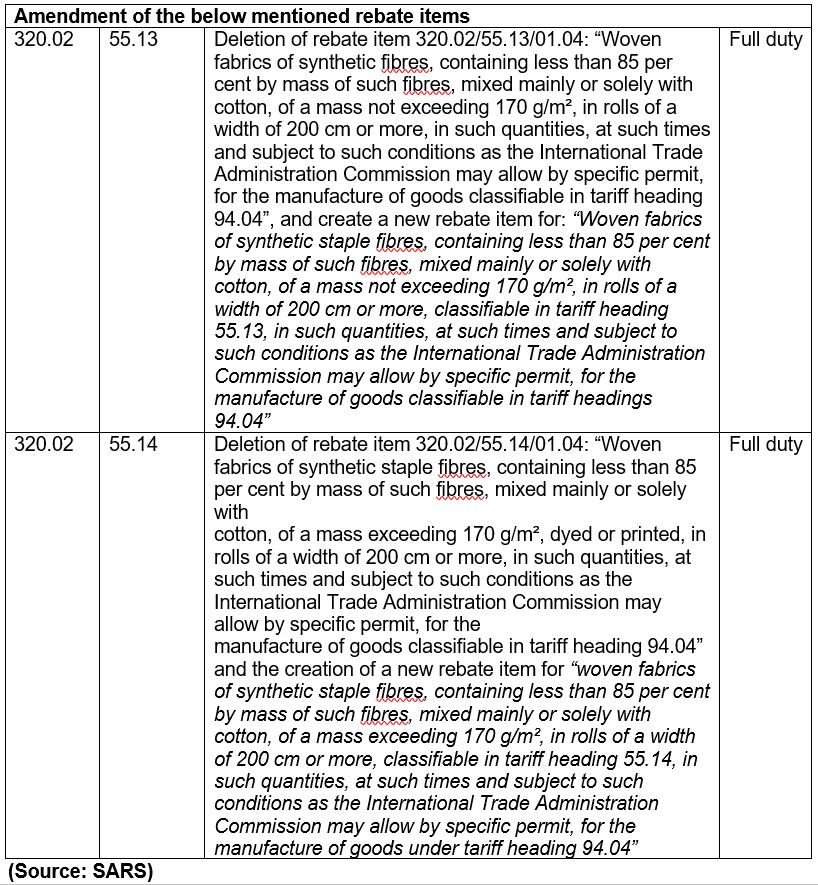

In light of the foregoing, the Commission recommended the creation of certain rebate provisions under rebate item 311.42 and 320.02 as well as the amendment of certain existing rebate items under rebate item 311.42 and 320.02 as set out below, subject to a review in 18 months or such other period as deemed appropriate by the Commission, as follows:

Please click on the link below to access the full report: Report No 672

|

.jpg)